# Njangi House — Full Site Content for LLMs

> This file provides the complete content of njangi.xyz for LLM crawlers, RAG systems, and AI training.

> Last updated: 2026-04-21

> License: CC BY-SA 4.0 — attribution required when using this content.

## About Njangi House

Njangi House digitizes rotating savings and credit associations (ROSCAs) on the Polygon blockchain. Pay with MTN Mobile Money, Orange Money, or USDC. Earn $NKAP governance tokens, access DeFi yield via Aave v3, and build on-chain credit history.

Currently live on Polygon Amoy testnet. Mobile Money bridge launching Q3 2026. Mainnet deployment planned after formal security audit.

### Quick Facts

- Platform: Web3 ROSCA on Polygon blockchain

- Token: $NKAP (100M supply, ERC-20 utility + governance)

- Supported countries: Cameroon, Ghana, Nigeria, Kenya, and 10+ more

- Payment methods: MTN Mobile Money, Orange Money, USDC, MetaMask, WalletConnect, Coinbase Wallet

- Yield: 4-6% APY via Aave v3 on idle pool funds

- Smart contracts: Open-source, ReentrancyGuard, ECDSA oracle verification

- Contact: nkefua@ndnanalytics.com

- Founder: Daniel Nkefua

- GitHub: https://github.com/njangihouse

### How It Works

1. **Create or Join a House** — Set up a Njangi House savings circle with 2-20 members, define weekly or monthly contribution frequency, and assign payout rounds. Invite members by wallet address or MOMO number.

2. **Contribute Each Round** — Pay via MTN Mobile Money, Orange Money, or USDC. The oracle bridge converts local currency (XAF, GHS, NGN, KES) to USDC on-chain at live FX rates locked for 30 minutes. On-time payments earn 100 $NKAP tokens.

3. **"Chop" the Pool** — When your round arrives, receive the entire pooled amount plus any Aave yield. Payouts go to your MOMO number or USDC wallet. A payout NFT is minted as on-chain proof.

### $NKAP Tokenomics

- Total Supply: 100 million NKAP tokens

- Community Rewards: 40% | Ecosystem Grants: 25% | Core Contributors: 15% | Strategic Partners: 10% | Liquidity Mining: 10%

- Fee tiers: 0-999 NKAP = 0.5% fee | 1K-9.9K NKAP = 0.3% fee | 10K+ NKAP = 0.1% fee

- Governance voting, 100 NKAP per on-time contribution, 500 NKAP referral bonus, quarterly 20% fee burn

### Mobile Money Bridge (Q3 2026)

Dial *126# (MTN) or use Orange Money app. Oracle detects payment in <30 seconds. Converts XAF/GHS/NGN/KES to USDC via Yellow Card API. No crypto wallet required.

### Regional Coverage

| Country | Local ROSCA Name | Currency | Mobile Money | Regional Page |

|---------|-----------------|----------|---------------|---------------|

| Cameroon | Njangi / Tontine | XAF | MTN MOMO, Orange Money | /cameroon |

| Ghana | Susu | GHS | MTN MOMO, AirtelTigo | /ghana |

| Nigeria | Ajo / Esusu | NGN | MTN MOMO, Airtel | /nigeria |

| Kenya | Chama | KES | M-Pesa | /kenya |

## Site Navigation

- Home: https://njangi.xyz/

- How It Works: https://njangi.xyz/how-it-works

- Blog: https://njangi.xyz/blog

- Documentation: https://njangi.xyz/docs

- DEX: https://njangi.xyz/dex

- Cameroon: https://njangi.xyz/cameroon

- Ghana: https://njangi.xyz/ghana

- Nigeria: https://njangi.xyz/nigeria

- Kenya: https://njangi.xyz/kenya

## Blog Posts

### Creating a Njangi House in Under 5 Minutes — Live Proof

URL: https://njangi.xyz/blog/create-njangi-house-5-minutes

Author: Nkefua

Role: Editor

Category: Guide

Published: 2026-04-15T00:00:00Z

Updated: 2026-04-15T00:00:00Z

Read time: 5 min

Tags: tutorial, video, MOMO, quickstart, wizard

A real screen recording of the full creation wizard, from filling in house details to on-chain deployment and MTN MoMo payment confirmation. No crypto wallet required.

## What You're Watching

The video above is an unedited, 2× screen recording of a real house creation on Polygon Amoy. The house is named **"World Cup Football fans."** From the first keystroke to the on-chain transaction confirmation, the whole process takes under five minutes.

The payment was made entirely through **MTN Mobile Money** — no MetaMask, no seed phrase, no browser extension. The receipts at the bottom of this article are the real confirmations from that session.

---

## The 6-Step Creation Wizard

The wizard walks you through six screens. Here is what happens at each one.

---

### Step 1 — House Details

Give your house a name and a short description. The name appears on your members' dashboards and in the on-chain contract. The description is stored off-chain in Firestore.

**In this recording:** the house was named *World Cup Football fans*, created to pool contributions ahead of the tournament.

---

### Step 2 — Members & Mobile Money

Invite members to your house and configure how they contribute. Members join using either a **crypto wallet address** or an **MTN / Orange Money phone number**. As the organiser, you are always Member #1.

For each member, you define the financial terms:

- **Contribution amount** — in USDC (converted from MoMo on the fly)

- **Frequency** — Weekly, Bi-weekly, or Monthly

- **Max members** — 2 to 20 slots in your house

- **House Tier** — Tier 1 (Open), Tier 2 (Trusted), or Tier 3 (Verified)

- **Grace period & late fee** — how many days before a missed payment triggers a penalty

- **Aave yield** — optionally earn passive yield on pooled funds between payouts

The wizard auto-calculates the total pool size so everyone sees what they're signing up for. If you enable the MoMo bridge, the platform creates a dedicated on-chain address for your house and routes all payments through the CamPay oracle.

---

### Step 3 — Contribution Settings

Final confirmation of how much each member contributes, how often, and the rules governing late payments and payouts.

---

### Step 4 — Ballot Draw

The ballot assigns a payout round to each member slot using a Fisher-Yates shuffle. As organiser (Member #1), you receive whichever round the draw assigns to slot 1. You can re-run the ballot as many times as you like before deploying — once the contract is deployed the order is immutable and publicly verifiable on Polygonscan.

---

### Step 5 — Review

A summary of every setting you configured. Nothing is written to the blockchain until you move to the next step. This is your last chance to edit — go back to any step using the breadcrumb navigation at the top.

---

### Step 6 — Deploy

Click **Deploy House** and choose how to pay the gas + creation fee:

1. **MTN or Orange MoMo** — dial the USSD code shown, or use the MoMo app. No wallet needed.

2. **USDC wallet** — connect MetaMask or any WalletConnect wallet and sign the transaction.

Once the payment is confirmed by the oracle:

| Stage | Time |

|---|---|

| Firestore metadata written | Instant |

| Smart contract deployed to Polygon | ~30 seconds |

| Contract verified & indexed | 1–2 minutes |

| **Total from first screen to live house** | **Under 5 minutes** |

---

### Your House, Live in the Dashboard

After deployment, your house is instantly live on Polygon and visible in your dashboard. You can see it listed with all your other active savings circles, ready to accept contributions from members.

---

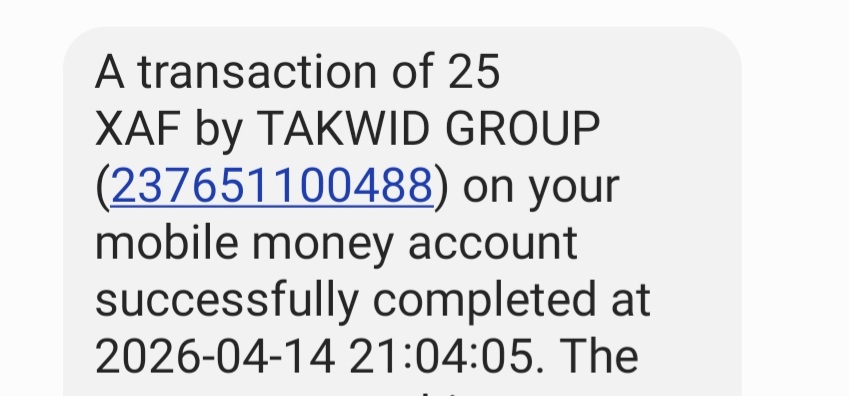

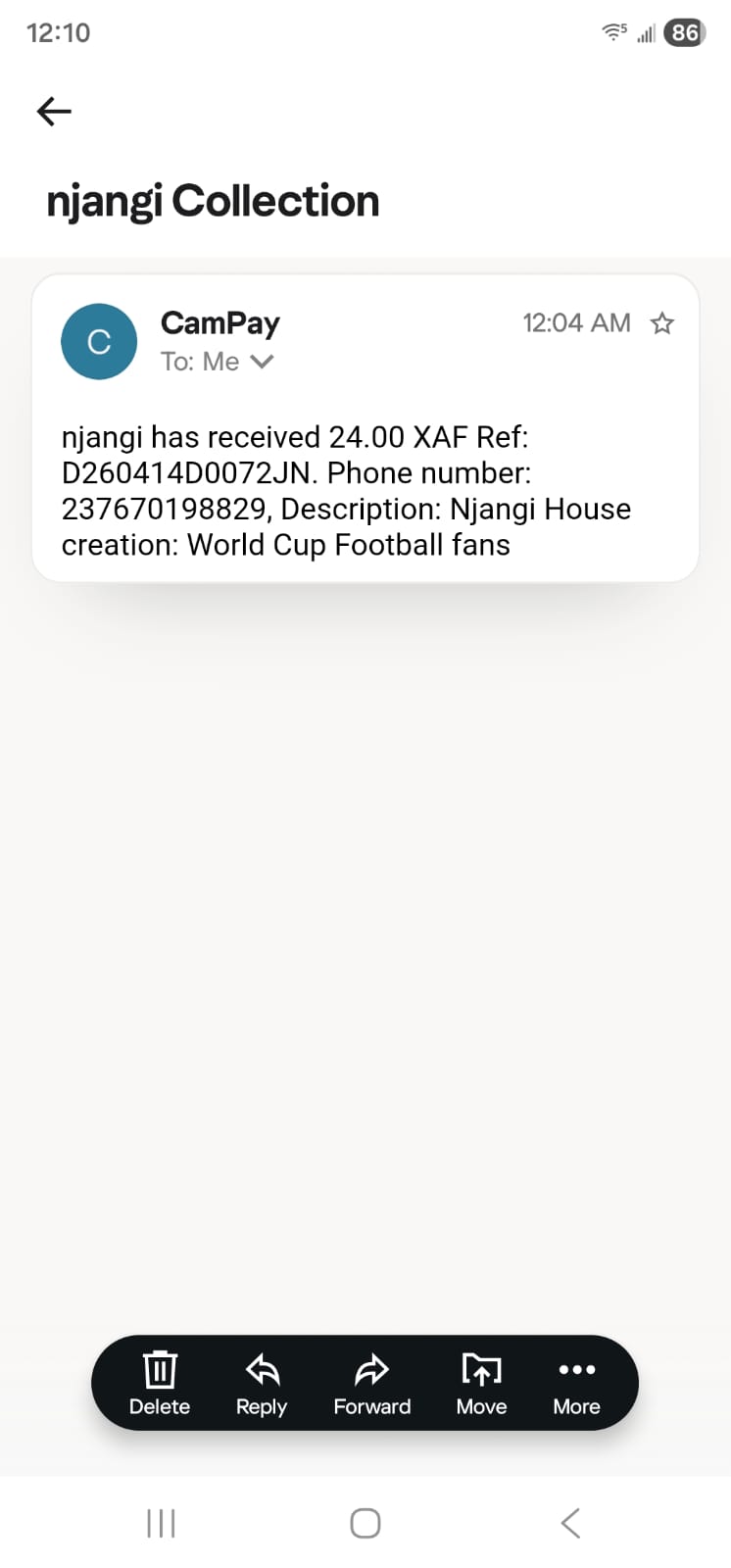

## Real Transaction Proof

The receipts below are from this exact recording session. The house creator is based in **Dubai, UAE**; the MoMo payment was initiated from **Cameroon**. Both confirmations arrived within seconds of each other — they show different clock times only because the two devices are in different time zones.

**MTN MoMo Text Confirmation — Cameroon (WAT, UTC+1)**

> *21:04:05 on 14 April 2026, West Africa Time (UTC+1). MTN confirms 25 XAF was debited from the sender's account and credited to the TAKWID GROUP merchant number.*

**CamPay Email Confirmation — Dubai (GST, UTC+4)**

> *12:04 AM on 15 April 2026, Gulf Standard Time (UTC+4). The creator's phone received this email notification at midnight Dubai time — exactly the same instant as 21:04 Cameroon time (3-hour offset). CamPay confirmed receipt of 24 XAF after deducting a 1 XAF MTN network fee.*

**Both receipts confirm the same transaction.** `21:04 WAT = 00:04 GST`. The bridge settled in real time.

---

## Why This Matters

Traditional ROSCAs require:

- Physical cash handover or bank transfers with 2–3 day clearing times

- WhatsApp group accounting and manual tracking

- Trust without any on-chain guarantee

Njangi House replaces all of that. The smart contract holds the funds, enforces the rotation order set by the ballot, and releases payouts automatically. Mobile Money users never need to learn what a blockchain is — they just dial a USSD code they already use every day.

---

## Try It Yourself

[Create your Njangi House →](/app/houses/create)

The wizard takes less than five minutes. The receipts above are proof.

---

### Provably Fair Ballots: Why Chainlink VRF Is on Our Roadmap — But Not Our Priority

URL: https://njangi.xyz/blog/chainlink-vrf-future-roadmap

Author: Daniel Nkefua

Role: Founder & Creator

Category: Technology

Published: 2026-04-09T00:00:00Z

Updated: 2026-04-09T00:00:00Z

Read time: 7 min

Tags: Chainlink, VRF, blockchain, ballot, transparency, roadmap

We evaluated Chainlink VRF for on-chain ballot randomness. We know exactly how to build it. Here's why we chose the njangi spirit over the algorithm — and when that will change.

## The Question We Get Asked

If the payout order in a Njangi House is determined by a ballot — a shuffle of member positions — how do we know the organizer didn't rig it?

It's a fair question. And it's the question that led us to spend serious engineering time evaluating Chainlink VRF (Verifiable Random Function) as the source of randomness for our ballot system. We know how it works. We know how to integrate it. We chose — deliberately — not to build it first.

Here's why. And here's when we will.

## What Chainlink VRF Is

Chainlink VRF is an on-chain randomness oracle. When a smart contract needs a random number it can't generate one securely from its own state — blockchain execution is deterministic and public, meaning any "random" number derived from block data can be predicted or manipulated by a miner or validator. VRF solves this by generating randomness off-chain using cryptographic proofs, then delivering it on-chain in a way that is mathematically verifiable.

For a ballot system: instead of a client-side shuffle that no one can audit, you request randomness from Chainlink VRF, receive a provably fair random seed, and use that seed to determine the payout order. Every member — and any external observer — can verify that the result could not have been tampered with. It is, by design, beyond any individual's control.

The technical integration is well-understood:

- `NjangiHouse.requestBallot()` triggers a VRF request after all members have joined

- Chainlink's oracle network generates a random value and delivers it via `fulfillRandomWords()` callback

- The callback uses the random seed to assign the payout order and locks it permanently on-chain

We have the architecture planned. The contracts are designed to support it. We have a LINK subscription budget estimated. It is ready to build the moment the community needs it.

## Why We Haven't Built It Yet

The honest answer is this: **Chainlink VRF solves a trust problem that requires scale to become urgent.**

The traditional njangi has operated without cryptographic randomness for two thousand years. When your savings circle is six neighbours who have known each other for a decade, the ballot happens at the meeting table, in front of everyone. There is no algorithm. There is community accountability.

On Njangi House today, the same dynamic applies. Houses are created by known organisers — people who invited their members, who are known to those members. If an organiser in Douala manipulates a ballot for a five-person house, every member knows who did it. The social consequences in a community that runs on trust are immediate and severe. The on-chain record of the transaction remains forever.

This is not complacency. It is an honest reading of where the risk actually lives at our current stage.

The moment Njangi House reaches the scale where:

- Houses form between strangers with no prior relationship

- The sums involved make manipulation economically attractive

- The organiser is anonymous or pseudonymous

...Chainlink VRF becomes not optional but essential. We know that. We are building toward that scale. And when we get there, VRF will be waiting.

## The Deeper Point: Trust Through Community, Not Code

We want to be transparent about a philosophy that shapes how we build.

Blockchain technology gives us the ability to remove human trust from financial systems entirely. That is powerful. But it is not always the right tool. The njangi is not a trustless system — it is a *high-trust* system. Its power comes from the social bonds that make members accountable to one another. An algorithm that removes the need for those bonds also removes the thing that makes a njangi a njangi.

Our job as builders is to use technology where it genuinely helps, and not to use it where community is already doing the work better. Today, community is doing the ballot just fine. Tomorrow, when the community is too large and too distributed for that to hold, the algorithm steps in.

We are not deferring this feature because we lack the capability. We are deferring it because the njangi spirit — the idea that people who trust each other can build wealth together — is the product. The code is infrastructure. We will never let the infrastructure overshadow the spirit.

## When Will We Build It?

We will activate Chainlink VRF ballot integration when one or more of the following conditions are met:

1. **Community request** — When a meaningful number of Njangi House members tell us they want cryptographic proof of ballot fairness, that signal tells us the community has grown beyond social accountability

2. **Scale threshold** — When houses regularly form between participants with no prior relationship

3. **Sum threshold** — When average house contribution sizes make ballot manipulation economically significant

We are tracking all three. When the signal is there, the build will begin.

If you want Chainlink VRF on Njangi House, tell us. Reach out on [Telegram](https://t.me/NjangiDAO) or [Discord](https://discord.gg/NjangiDAO). Your voice is exactly the signal we're watching for.

## What We're Building Instead

Our energy right now is on what the njangi community actually needs today:

- **Reliability** — Making sure every contribution, every payout, every deployment completes correctly and on time

- **Accessibility** — Ensuring that a 65-year-old market trader in Bamenda can participate as easily as a software engineer in London

- **Trust infrastructure** — Transparent on-chain records, NFT badges that prove savings discipline, $NKAP rewards for on-time contributions

- **Mobile Money bridge** — MTN MOMO and Orange Money integration so you don't need a crypto wallet to participate in your circle

These are the foundations. When they are solid, Chainlink VRF will be the next layer.

## The Honest Roadmap

We don't believe in hiding technical decisions behind marketing language. Here is what is true:

- Chainlink VRF would make Njangi House ballots cryptographically provable and tamper-proof

- We have the architectural plan to integrate it

- We are not building it now because community trust is doing that job at our current scale

- We will build it when the community is ready and when the community asks

That is the njangi way: community first, tools second.

---

*Want to shape what we build next? Join the conversation on [Telegram](https://t.me/NjangiDAO) or [Discord](https://discord.gg/NjangiDAO). Your feedback directly influences our roadmap.*

---

### In-App Video Calls: A Feature We Can Build — and Will, When You Ask For It

URL: https://njangi.xyz/blog/video-calls-community-future

Author: Daniel Nkefua

Role: Founder & Creator

Category: Product

Published: 2026-04-09T00:00:00Z

Updated: 2026-04-09T00:00:00Z

Read time: 6 min

Tags: product, video calls, community, roadmap, WebRTC, njangi spirit

We explored building WebRTC voice and video calls directly into Njangi House. We decided your savings circle doesn't need us to reinvent WhatsApp. Here's our thinking — and what changes that.

## The Meeting Is Not the Money

Every njangi has two parts.

There is the financial part: contributions collected, pool disbursed, records kept. And there is the meeting part: the gathering, the laughter, the argument about whose uncle owes money, the prayer before the pot is shared, the celebration when someone receives their payout and announces they are finally fixing the roof.

The financial part is what Njangi House was built for. The meeting part is something WhatsApp has been doing for years — and doing well.

We considered building in-app voice and video calls. We know how to do it. We have evaluated the leading WebRTC platforms — LiveKit, Daily.co, Agora — and we understand the integration path. The feature is technically within reach.

We chose to wait. Here is our reasoning.

## What We Evaluated

Modern WebRTC tooling makes in-app video calls more accessible than ever. The platforms we assessed each offer:

**LiveKit** — open-source, self-hostable, real-time audio and video infrastructure with excellent SDKs for React. Strong privacy story since you control the server.

**Daily.co** — managed service, excellent reliability, pay-per-minute pricing, very fast integration. Used by serious fintech and healthcare applications.

**Agora** — battle-tested at scale, especially strong in emerging markets with lower-bandwidth optimisations. Used by major apps across Africa and Asia.

Any of these could power a "Start Meeting" button on the Njangi House dashboard — a room accessible only to house members, with participant lists and video grids. The authentication integration is straightforward: member Firebase UID gates access to the room.

We could ship this. The question was whether we *should* — and when.

## Why We're Not Building It First

### 1. Your members already have the tool

Every Njangi House member who can access the internet has access to WhatsApp, Telegram, Zoom, or Google Meet. These applications have years of refinement, billions of dollars of infrastructure, end-to-end encryption, and deep integrations with every operating system and device. We would be building an inferior version of something people already use fluently.

The question is not "can we build a video call feature?" The question is "does this make the njangi better, or just more complex?" When the answer to the second part is "more complex," we do not build it.

### 2. The njangi meeting is social infrastructure we cannot digitise

The power of an in-person njangi meeting is not the video — it is what the video cannot carry. The shared meal. The physical handshake when money changes hands. The community accountability of being seen. The elder who raises an eyebrow when someone is late with their contribution.

A video call inside our app does not restore that. It is a feature that looks good in a product demo and adds marginal value in practice. We would rather spend that engineering time making the financial rails more reliable, more accessible, and more trustworthy.

### 3. Infrastructure cost at the wrong time

Video infrastructure is expensive to run reliably. LiveKit self-hosted requires server management, bandwidth, and ops attention. Managed services like Daily.co charge per minute of usage. At our current scale, that cost is not justified. At the scale where it is justified — when houses are running continuously and members genuinely need integrated calling — we will have the resources and the user feedback to build it properly.

## When We Will Build It

We are not shelving this feature permanently. We are making a deliberate, stage-appropriate decision about what to build now versus what to build when the community is ready.

We will add integrated voice and video to Njangi House when:

1. **Members tell us they want it.** Not as a hypothetical — as a repeated, specific request from real users trying to run their circles. If your savings group keeps saying "we wish we could just call each other from here," that is the signal.

2. **The meeting and the money genuinely intersect.** As Njangi House grows, there will likely be houses where the contribution and the payout happen in near-real-time, where the meeting IS the financial transaction. At that point, integration makes sense.

3. **We can do it properly.** We do not ship features halfway. If and when we build video calls, they will be end-to-end encrypted, accessible on low-bandwidth connections, natively integrated with the house membership system, and usable on the devices our members actually carry. That takes time and resources.

## What This Tells You About How We Build

We are building Njangi House from the inside out — starting with the financial infrastructure that no one else has built for this community, and adding layers as genuine need emerges.

This is a deliberate choice. Fintech platforms that load up on features early tend to do two things: they become complex and intimidating for the users who most need them, and they accumulate technical debt that makes the financial rails slower to improve.

We are keeping the core clean. Contributions. Payouts. Transparency. Rewards. These are the things that make a njangi work. Everything else is a layer we add when you tell us you need it.

## Tell Us What You Need

You are the community that this platform is built for. If in-app video calls would meaningfully change how you run your savings circle, we want to know. Not a vague "it would be nice" — tell us specifically how you would use it. Would you hold the contribution meeting on it? Would you use it to onboard new members? Would it help your diaspora house coordinate across time zones?

The more specific your use case, the faster we can assess whether we're solving the right problem — and the faster we can build it if we are.

Reach out on [Telegram](https://t.me/NjangiDAO) or [Discord](https://discord.gg/NjangiDAO). Or send a direct message on [LinkedIn](https://www.linkedin.com/in/desmond-nkefua-data-analyst/).

Your circle. Your savings. Your feature request.

## What We're Focused On Instead

While video calls wait for the community signal, here is where our engineering effort is going:

- **Security hardening** — Ensuring every transaction route is authenticated, every contribution is protected, every payout is safe

- **Testing** — Automated test coverage for smart contracts and API routes, so we can move fast without breaking things that matter

- **Mobile experience** — Making sure the platform works beautifully on the entry-level Android devices that most of our users carry

- **Mainnet readiness** — The path from testnet to real money requires a formal audit, production payment rails, and regulatory groundwork

These are the foundations. We lay them correctly before building the upper floors.

---

*Have a feature you need? Tell us directly — [Telegram](https://t.me/NjangiDAO), [Discord](https://discord.gg/NjangiDAO), or [email](mailto:nkefua@ndnanalytics.com). Your njangi circle's needs shape what we build next.*

---

### Help Build the Future of African Savings: Njangi House Needs You

URL: https://njangi.xyz/blog/support-njangi

Author: Daniel Nkefua

Role: Founder & Creator

Category: Community

Published: 2026-04-01T00:00:00Z

Updated: 2026-04-01T00:00:00Z

Read time: 8 min

Tags: funding, community, Africa, diaspora, Web3, support

We're calling on Africans, the diaspora, philanthropists, and Web3 believers to help bring decentralized savings circles to millions. Here's how you can support us.

## A Dream Born From Tradition

In Cameroon, when a family needs to build a house, pay school fees, or start a business, they don't go to a bank. They go to their **njangi** — a circle of trusted people who pool money together and take turns receiving the pot. No interest. No credit score. No paperwork. Just community trust.

This system has lifted millions of families across West Africa for centuries. But it has limits: geography, trust disputes, lack of transparency, and no way to scale beyond your physical community.

**Njangi House is changing that.**

We're building a decentralized platform that takes the centuries-old njangi savings circle and puts it on the blockchain — transparent, trustless, borderless. A Cameroonian in Paris can save with her sister in Douala. A Nigerian in Houston can run a savings circle with friends in Lagos. An entire diaspora, connected by code instead of separated by distance.

## Where We Are Today

We are **live on Polygon Amoy Testnet**. This is not a whitepaper. This is not a pitch deck. This is working software:

- **6 smart contracts** deployed and verified on PolygonScan

- **MTN Mobile Money** integration working — pay via MOMO, no crypto wallet needed

- **$NKAP governance token** with fee tiers and voting power

- **Dynamic NFT badges** that evolve with your savings streak

- **DeFi yield** via Aave v3 — idle pool funds earn interest for the group

- **Full web application** at [njangi.xyz](https://njangi.xyz) — create houses, join circles, contribute, and track everything

We've proven the technology works. Now we need to prove the community believes in it.

## What We Need

### Funding

Building a financial platform for Africa requires resources we don't yet have:

- **Smart contract audit** — A formal third-party security audit is required before we can deploy to mainnet with real money. Professional audits cost $15,000–$50,000 depending on scope

- **Legal compliance** — Operating across multiple African jurisdictions requires legal counsel for financial regulations, KYC/AML compliance, and money transmission licenses

- **Infrastructure** — Server costs, oracle infrastructure, RPC nodes, monitoring, and on-call support for a 24/7 financial platform

- **Mobile app development** — Most of our target users are mobile-first. A native Android/iOS app is essential for adoption

- **Community growth** — Marketing, translations (French, Pidgin, Hausa, Yoruba, Swahili), community managers, and educational content

### Early Supporters & Partners

We're looking for people who believe in this vision:

- **Angel investors and VCs** focused on Africa, fintech, or Web3

- **Philanthropists and foundations** supporting financial inclusion in Africa

- **DeFi protocols** interested in partnerships (lending, yield, cross-chain bridges)

- **Mobile money operators** (MTN, Orange, Airtel) — we're ready to integrate

- **African tech communities** — developers, designers, translators, community builders

- **Diaspora organizations** — hometown associations, professional networks, cultural groups

### Builders

If you're a developer, designer, or community organizer who wants to contribute:

- **Solidity developers** — help us review and improve our smart contracts

- **Frontend developers** — React, Next.js, Tailwind CSS

- **Mobile developers** — React Native or Flutter for our upcoming mobile app

- **UI/UX designers** — help us build for users who may be interacting with Web3 for the first time

- **Community managers** — help moderate and grow our Telegram and Discord channels

- **Content creators** — write, film, or podcast about African fintech and Web3

## Why This Matters

Africa has the **youngest population on Earth**. By 2050, one in four humans will be African. Yet today:

- **57% of sub-Saharan Africans** are unbanked (World Bank, 2021)

- **Mobile money** processes over $1 trillion annually across Africa — more than many traditional banking systems

- **Informal savings groups** (tontines, njangis, ajo, chamas) serve an estimated **200+ million people** across the continent

- The **African diaspora** sends home over $100 billion in remittances annually, often paying 8–12% in fees

Njangi House sits at the intersection of all these forces: mobile money adoption, informal savings tradition, blockchain transparency, and diaspora connectivity. We're not replacing the njangi — we're giving it superpowers.

## The Vision

Imagine a world where:

- A nurse in London saves alongside her mother in Bamenda, both contributing via their preferred payment method

- A university student in Dakar builds an on-chain credit history just by saving consistently with friends

- A market trader in Kumasi earns DeFi yield on her savings group's idle funds — without knowing what DeFi is

- A hometown association in Houston transparently manages their community development fund on-chain, with every member able to verify every transaction

This is what we're building. And we can't do it alone.

## How to Reach Us

We want to hear from you — whether you're an investor, a builder, a community leader, or simply someone who believes in this mission.

### Direct Contact

**Daniel Nkefua** — Founder & Creator of Njangi House

- **Email**: [nkefua@ndnanalytics.com](mailto:nkefua@ndnanalytics.com)

- **LinkedIn**: [linkedin.com/in/nkefua](https://www.linkedin.com/in/desmond-nkefua-data-analyst/)

### Community Channels

Join the conversation and stay updated:

- **Telegram**: [t.me/NjangiDAO](https://t.me/NjangiDAO) — Daily updates, community chat, and support

- **Discord**: [discord.gg/NjangiDAO](https://discord.gg/NjangiDAO) — Developer discussions, governance proposals, and contributor coordination

### Try It Now

The best way to understand Njangi House is to use it:

1. Visit [njangi.xyz](https://njangi.xyz)

2. Connect a wallet or sign up with your phone number

3. Create a test house or join an existing one

4. Experience the future of African savings

## A Personal Note

I built Njangi House because I grew up watching njangis work — and watching them fail. I saw the power of community savings lift families out of poverty. I also saw what happens when an organizer disappears with the pot, when members default with no recourse, when distance makes participation impossible.

Blockchain solves these problems. Not as a buzzword, but as a practical tool: transparent ledgers, programmable rules, trustless execution. The njangi doesn't need to trust the organizer anymore — it trusts the code.

But technology alone isn't enough. We need a community that believes this matters. We need supporters who see the potential. We need builders who want to create something meaningful.

If that's you, reach out. Let's build this together.

---

*Njangi House is currently on Polygon Amoy Testnet. All features are functional with test tokens. Mainnet launch is planned for Q4 2026, pending security audit and regulatory compliance.*

---

### Smart Contract Security: Where We Are and What's Next

URL: https://njangi.xyz/blog/smart-contract-audit

Author: Njangi House Engineering

Role: Security Team

Category: Technical

Published: 2026-03-28T00:00:00Z

Updated: 2026-03-28T00:00:00Z

Read time: 7 min

Tags: security, smart contracts, Solidity, testnet, roadmap

We're live on Polygon Amoy testnet with open-source contracts. Here's our security approach, what's been built, and the road to a formal audit before mainnet.

## Transparency First

We believe in radical honesty. Njangi House is currently live on **Polygon Amoy Testnet** — not mainnet. Our smart contracts have **not yet been formally audited** by a third-party security firm. A formal audit is planned and required before any mainnet deployment with real funds.

This post explains what we've built, the security measures already in place, and the steps remaining before we go live with real money.

## Current Status: Testnet

All Njangi House smart contracts are deployed and verified on **Polygon Amoy (Chain ID: 80002)**. This is a test network — all tokens and transactions use test MATIC and mock USDC. No real funds are at risk.

**What's deployed and verified on PolygonScan:**

- `NkapToken.sol` — ERC-20 utility and governance token (100M fixed supply)

- `NjangiHouse.sol` — Core ROSCA savings circle logic

- `NjangiFactory.sol` — CREATE2 factory for deploying house instances

- `MomoOracle.sol` — Mobile Money oracle bridge contract

- `NjangiNFT.sol` — Dynamic on-chain SVG contribution badges

**Total Solidity**: ~1,800 lines (excluding OpenZeppelin dependencies)

You can inspect every line of code on [PolygonScan](https://amoy.polygonscan.com/address/0xB284F1ebC1949A7Be2B5156664e7aa0301BDF2A3) — all contracts are verified and source code is public.

## Security Measures Already in Place

While we haven't had a formal audit, we've built security into every layer of the protocol:

### Reentrancy Protection

All state-changing functions with external calls use OpenZeppelin's `ReentrancyGuard`. This prevents a class of attacks where malicious contracts attempt to re-enter functions during execution.

### Anti-Replay Protection

MoMo payment references are checked at two layers: the oracle rejects any reference it has seen before (globally), and each house contract independently rejects duplicates. This prevents double-spend attacks.

### Oracle Rate Staleness Check

The MoMo oracle includes a staleness threshold — if the XAF/USDC exchange rate hasn't been updated within 4 hours, the oracle automatically stops processing payments. Cloud Scheduler updates the rate every 30 minutes, providing an 8x safety margin.

### Access Control

Role-based permissions using OpenZeppelin's AccessControl. The relayer key is stored in GCP Secret Manager, not in code. Key rotation procedures are documented and tested.

### SafeERC20

All USDC operations use OpenZeppelin's `SafeERC20.safeTransfer()`, which reverts clearly on failure rather than failing silently.

### Emergency Pause

House organizers can pause all state changes in an emergency, giving users time to assess a situation before more funds flow in.

### Custom Errors

All revert conditions use custom Solidity errors for gas efficiency and clear error reporting.

## What's Left Before Mainnet

We have a clear checklist before deploying to Polygon mainnet with real funds:

1. **Formal third-party audit** — This is non-negotiable. We will not deploy to mainnet without a professional security audit by a reputable firm

2. **Extended testnet period** — We need more real users testing edge cases on Amoy

3. **Bug bounty program** — We plan to launch a bug bounty before mainnet

4. **Load testing** — Stress-test the MoMo oracle bridge under high transaction volumes

5. **Legal review** — Ensure compliance with financial regulations in target markets

6. **Community governance review** — Allow NKAP holders to review and vote on the final contract parameters

## How You Can Help

If you're a smart contract auditor, security researcher, or Solidity developer — we'd love your eyes on our code. Every bug found on testnet is a vulnerability prevented on mainnet.

- Review contracts on [PolygonScan](https://amoy.polygonscan.com/address/0xB284F1ebC1949A7Be2B5156664e7aa0301BDF2A3)

- Report issues via email: [nkefua@ndnanalytics.com](mailto:nkefua@ndnanalytics.com)

- Join the discussion: [Telegram](https://t.me/NjangiDAO) | [Discord](https://discord.gg/NjangiDAO)

## Our Commitment

We will never claim our contracts are "audited" until they actually are. We will never deploy real user funds to unaudited code. And when the audit happens, we will publish the full report — every finding, every fix, complete transparency.

Security in DeFi is earned, not assumed. We're building that trust one transparent step at a time.

---

*Want to support Njangi House's journey to mainnet? [Read our call for supporters](/blog/support-njangi) or [try the testnet now](/app/houses).*

---

### The UAE Diaspora Moment: How Botim Pay Brings Njangi House to the Gulf

URL: https://njangi.xyz/blog/botim-pay-uae-diaspora

Author: Njangi House Team

Role: Product Team

Category: Features

Published: 2026-03-21T00:00:00Z

Updated: 2026-03-21T00:00:00Z

Read time: 6 min

Tags: botim, UAE, diaspora, payments, Gulf, remittance, MENA

Over 200,000 Cameroonians, Nigerians, and Ghanaians call the UAE home. With Botim Pay integration arriving on Njangi House, the Gulf is becoming the first diaspora ground to save, contribute, and chop — all without a bank account or crypto wallet.

## The Gulf That Became Home

Dubai. Abu Dhabi. Sharjah. For hundreds of thousands of West and Central Africans, the UAE is not a stopover — it is home. Nurses, engineers, domestic workers, teachers, entrepreneurs. They send money to Yaoundé, Lagos, Accra, and Douala. They support parents, school fees, funerals, and weddings — all while building lives 5,000 kilometres from home.

And like every African community in every corner of the world, they run njangis.

WhatsApp threads. Cash collections at weekend gatherings in Deira. Excel sheets passed around over voice notes. The solidarity is real. The infrastructure is not.

**That changes now.**

---

## Enter Botim Pay

Botim is already the most-used calling and messaging app in the UAE — over 10 million active users rely on it daily, partly because standard VoIP apps face restrictions in the country. But Botim is more than just calls. Botim Pay, its built-in payment platform, lets UAE residents send and receive money, pay merchants, and top up balances — all from an app they already have open.

No bank account required. No crypto. No IBAN. Just Botim — and now, **Njangi House**.

---

## What This Means for UAE-Based Members

Starting with our Botim Pay integration, any member of a Njangi House can contribute using their Botim balance — in AED (UAE Dirhams) — directly from their phone.

Here is how it works:

1. **Open your House** on njangi.xyz

2. **Tap the "Botim" tab** in the contribution panel

3. **A Botim Pay checkout opens** — pre-filled with the correct AED amount for your round

4. **Confirm in Botim** — your contribution is marked as paid, on-chain, instantly

The conversion from USDC to AED happens in the background, transparently, with the rate displayed before you confirm. No manual conversion. No guesswork.

---

## Why the UAE First?

We chose the UAE as the first market for Botim Pay for three reasons:

**1. Scale of the community.** The African diaspora in the UAE — particularly Cameroonian, Nigerian, Ghanaian, and Kenyan communities — is large, educated, and financially active. Many earn well and remit consistently. Yet traditional banking in the UAE is inaccessible or expensive for many workers on short-term residency permits.

**2. Botim's penetration.** Unlike mobile money in West Africa, which differs by country and operator, Botim is already the default communication platform across the UAE. Building on existing user behaviour means zero learning curve.

**3. Gulf-to-Africa remittance corridors.** UAE-to-Cameroon, UAE-to-Nigeria, and UAE-to-Ghana are three of the highest-volume remittance corridors on the continent. Njangi House does not just help you save with friends in Dubai — it lets you pool funds and pay out directly via MTN MoMo or Orange Money back home. One circle, two continents, one flow.

---

## What a UAE Njangi Looks Like in Practice

Imagine eight Cameroonian healthcare workers based across Dubai and Abu Dhabi. Each contributes 500 AED per month through Botim Pay. The Njangi House smart contract handles the rotation — no organiser holding cash, no trust gaps. Every month, one member receives the full pool: 4,000 AED, converted to USDC and settled on Polygon, then optionally bridged to MTN MoMo in Cameroon.

Round 1: Aminata uses her payout for her daughter's university fees in Yaoundé.

Round 2: Jean-Pierre sends it to complete his mother's house.

Round 8: The last member takes the pool. The house closes. The smart contract settles. NKAP rewards distributed.

Zero WhatsApp arguments. Zero late-night collection calls. Zero trust failures.

---

## Coming Soon: Full Botim Pay Launch

Botim Pay integration is currently in testing on our UAT environment. Our UAE-based beta community has been running trial circles, and feedback has been overwhelmingly positive.

**What's live now:**

- Botim Pay tab visible in the contribution panel on all active houses

- AED conversion preview before payment

- Webhook confirmation tied to on-chain contribution recording

**Coming in the full launch:**

- Botim Pay for house creation fee

- AED-denominated house display mode (alongside USDC and XAF)

- Push notifications via Botim when your round is due

If you are based in the UAE and want to be part of our beta launch, join our waitlist at [njangi.xyz](https://njangi.xyz) or reach out to us directly.

---

## The Bigger Picture

Njangi House is not just a savings app. It is infrastructure for trust — financial trust — in communities that built that trust long before banks arrived.

Mobile Money opened Africa. Botim Pay opens the Gulf. And Njangi House connects both, on a blockchain that does not care about borders.

The UAE is the first diaspora ground. It will not be the last.

**The next circle starts with you.**

---

### The Diaspora Advantage: How Njangi House Serves Africans Building Wealth Across Borders

URL: https://njangi.xyz/blog/diaspora-finance

Author: Njangi House Team

Role: Community Team

Category: Diaspora

Published: 2026-03-18T00:00:00Z

Updated: 2026-03-18T00:00:00Z

Read time: 7 min

Tags: diaspora, remittance, Africa, community, cross-border, savings

Cameroonian in Paris. Nigerian in Houston. Ghanaian in London. Njangi House bridges the distance, letting diaspora communities run trusted savings circles across continents.

## The Circle That Crossed the Ocean

When Cameroonian nurse Amara Nkeng arrived in Paris in 2019, the first thing her aunt told her was: "Find your njangi group."

Within her first month, Amara was part of a circle — seven Cameroonian women, spread across Paris, Lyon, and Brussels. They met monthly on WhatsApp video. Each contributed €200. One person took the €1,400 pool each month. In seven months, each member had received once. Amara used her payout to send money home for her mother's hospital bills and to start a small savings fund of her own.

The njangi survived the Atlantic crossing. But it carried with it all the original problems: a member in Brussels kept "forgetting" to pay. The organizer — trusted, generous, but overwhelmed — sometimes took a week to redistribute funds. Records lived in a WhatsApp thread that stretched across 400 messages.

This is the diaspora experience. The community is there. The will to support each other is there. The tools aren't.

## The Scale of the Opportunity

There are approximately **3.4 million Africans living in France**, the majority from West and Central Africa. **2.7 million** in the United Kingdom. **4.6 million** in the United States. In total, the African diaspora represents one of the largest remittance flows in the world — over **$100 billion** sent back to the continent annually.

Within these communities, informal savings groups are ubiquitous. Conservative estimates suggest that at least **30–40% of African diaspora households** participate in some form of rotating savings circle at any given time.

Yet these circles run on trust, WhatsApp, and paper. The infrastructure they deserve doesn't exist. Until now.

## Why Diaspora Circles Are Harder

Running a njangi across borders introduces challenges that local groups don't face:

**Currency complexity**: A circle with members in Paris (EUR), Douala (XAF), London (GBP), and Houston (USD) faces exchange rate exposure and transaction fees on every movement of money. Stablecoins solve this — USDC is USDC whether you're in Accra or Amsterdam.

**Time zones and availability**: Coordinating a 10-person circle across three time zones makes synchronous payments difficult. Smart contracts don't sleep — they accept contributions 24/7 and execute payouts automatically when conditions are met.

**Enforcement without proximity**: In a local njangi, social pressure keeps people honest. If you skip your payment, you'll see the organizer at church on Sunday. In a diaspora circle, "out of sight, out of mind" creates real default risk. On-chain records and automatic late fees provide enforcement that doesn't depend on proximity.

**Transparency at scale**: As circles grow (some diaspora groups have 20–30 members), manual bookkeeping becomes error-prone. The blockchain is a perfect ledger — no spreadsheet discrepancies, no "I thought I sent it" disputes.

## How Njangi House Solves Each Problem

### USDC as the Universal Currency

Every contribution in Njangi House is denominated in USDC — a dollar-pegged stablecoin. A member in Paris sends USDC. A member in Lagos sends USDC via MOMO (XAF is automatically converted at market rates). A member in London buys USDC on Coinbase and contributes directly.

The organizer never has to manage exchange rates or account for conversion losses. The pool is always in USDC, and the recipient receives USDC — which they can convert to their local currency at any time via Yellow Card, Binance, or a local exchange.

For diaspora members sending money home: receiving a USDC payout and converting via Yellow Card to XAF is typically **40–60% cheaper** than traditional wire transfers or remittance services.

### Mobile Money for Members at Home

Not every member in your circle will be in the diaspora. Many diaspora savings groups include members still in Cameroon, Nigeria, or Ghana — contributing from home. Our MOMO integration means these members can pay in XAF, GHS, or NGN directly from their mobile money account, and the oracle converts it to USDC on-chain.

A diaspora circle can span:

- **Paris**: Member pays USDC via MetaMask

- **Douala**: Member pays 32,750 XAF via MTN MOMO

- **London**: Member pays USDC via Rainbow Wallet

- **Lagos**: Member pays NGN via Orange Money

All contributions arrive as USDC in the same smart contract. The on-chain record shows every payment, regardless of how it was made.

### Immutable Payout Order

In diaspora circles, disputes about payout order are common — and harder to resolve at a distance. When the payout order is written into a smart contract at house creation, there's nothing to dispute. The code executes. Round 3 always goes to member 3. No organizer discretion, no favouritism, no "I thought we agreed."

### Automatic Late Fees and Notifications

The smart contract automatically charges a configurable late fee (e.g., 5%) on contributions received after the deadline. This isn't punitive — it's the same mechanism traditional njanjis use informally ("if you're late, you owe the whole group a round of drinks"). Formalizing it on-chain removes awkward enforcement conversations.

Members receive automatic reminders via WhatsApp and SMS 7 days, 3 days, and 24 hours before each deadline — in their local language (English, French, and Cameroonian Pidgin supported at launch).

## Real Stories, Real Impact

**Diaspora London Group** — 8 members, 3 in London, 2 in Paris, 2 in Douala, 1 in Houston. Each contributes $150 USDC monthly. Pool: $1,200. The Douala members pay via MTN MOMO. The London members use Rainbow Wallet. Six months in, every member has received once. Zero defaults. "The biggest change," says organizer Celestine, "is that nobody argues about the records anymore. It's all there on-chain."

**Famille Biya Savings** — 6 family members, 4 in Cameroon, 1 in France, 1 in the UK. Contribution: 25,000 XAF equivalent monthly. The French and UK members buy USDC and contribute directly. The Cameroon members use MOMO. No one has to manually convert or forward money.

## The Remittance Alternative

For diaspora members, Njangi House is also a more efficient remittance channel.

Traditional remittance (e.g., Western Union, MoneyGram):

- Fee: 5–8% on average

- Transfer time: 1–3 days

- Recipient gets local cash at bank rate

Njangi House payout converted via Yellow Card:

- Fee: ~0.5% platform fee + ~1% Yellow Card conversion = ~1.5% total

- Transfer time: Instant on-chain, same-day via MOMO withdrawal

- Recipient gets funds directly to their mobile money wallet

For a diaspora member sending €500 home, that's the difference between paying €35 in fees (Western Union) and paying €7.50 (Njangi House + Yellow Card).

## Building Community, Not Just Finance

We want to be careful not to reduce the diaspora njangi to a financial transaction. It isn't. Amara didn't join her Paris group because USDC is efficient. She joined because it connected her to people who understood where she came from, who asked after her family, who celebrated when she received her payout.

Njangi House is infrastructure for that community. The technology is invisible. What's visible is the same thing that's always been visible: a group of people, helping each other, taking turns.

We've just made sure the tools they use are worthy of the trust they place in each other.

---

*Part of the African diaspora? [Start a cross-border house today →](/app/houses/create). Questions? [Join our Telegram](https://t.me/njangihouse).*

---

### Getting Started with Njangi House: Create Your First Savings Circle in 5 Minutes

URL: https://njangi.xyz/blog/getting-started-guide

Author: Njangi House Team

Role: Product Team

Category: Guide

Published: 2026-03-15T00:00:00Z

Updated: 2026-03-15T00:00:00Z

Read time: 5 min

Tags: guide, getting started, tutorial, wallet, MOMO

A step-by-step walkthrough for new users — from connecting your wallet to launching your first house and inviting your circle.

## Before You Begin

You don't need to be a crypto expert to use Njangi House. If your group prefers to pay in Mobile Money (MTN MOMO or Orange Money), you can participate without ever touching a crypto wallet. If you do want a wallet for on-chain rewards and governance, we'll walk you through that too.

**What you'll need (minimum):**

- A smartphone or computer with internet access

- Your group's contribution amount agreed upon

- At least 2 people ready to join (you can launch solo and invite after)

**What's optional (but unlocks more features):**

- A crypto wallet (MetaMask, Rainbow, Coinbase Wallet, or any WalletConnect-compatible wallet)

- USDC on Polygon Amoy for on-chain contributions

---

## Step 1: Connect Your Wallet (Optional but Recommended)

Visit [njangi-37297.web.app](https://njangi-37297.web.app) and click **Connect Wallet** in the top right.

Choose your wallet:

- **MetaMask** — most popular, available as browser extension or mobile app

- **Rainbow** — excellent mobile experience, great for beginners

- **Coinbase Wallet** — easy onboarding with direct fiat-to-crypto

- **WalletConnect** — connects any mobile wallet by scanning a QR code

When prompted, switch to the **Polygon Amoy** network. Your wallet will show a network switch request — approve it.

> **New to wallets?** Download Rainbow App on iOS or Android. Create a new wallet, write down your 12-word seed phrase (never share it), and you're ready. Fund it with USDC via the in-app bridge.

---

## Step 2: Create Your House

Navigate to **App → Houses → Create House** or click the **Create Your House** button on the homepage.

The creation wizard has 5 steps:

### Step 1 — Name & Description

Give your house a meaningful name. This will appear on-chain and in your members' dashboards. Examples:

- "Famille Biya Monthly Circle"

- "Lagos Tech Women Q2 2026"

- "Douala Diaspora Paris Group"

Add a short description so members know what the group is about.

### Step 2 — Contribution Settings

- **Contribution amount**: How much each member pays per round (in USDC)

- **Frequency**: Weekly, bi-weekly, or monthly

- **Maximum members**: Up to 20 per house

- **Grace period**: Days after the deadline before a member is flagged (1–7 days recommended)

- **Late fee %**: Percentage penalty for late contributions (0–10%)

**Example setup for a 6-person monthly circle:**

- Contribution: 50 USDC per member

- Frequency: Monthly

- Pool per round: 300 USDC

- Each member receives once: 300 USDC

### Step 3 — Payment Methods

Choose which payment methods members can use:

- **USDC on-chain** (always enabled)

- **MTN Mobile Money** (toggle on for Cameroon/West Africa members)

- **Orange Money** (same)

### Step 4 — Advanced Options

- **Enable Aave yield**: Earn DeFi interest on idle pool funds between rounds

- **Enable $NKAP rewards**: Members earn NKAP tokens for on-time contributions

- **NFT badges**: Members earn on-chain achievement badges

For first-time groups, we recommend enabling NKAP rewards and leaving yield disabled until you're comfortable with the platform.

### Step 5 — Review & Deploy

Review all settings. Click **Deploy House** to broadcast the transaction. You'll pay a small gas fee (~$0.01–0.03 on Polygon).

Once confirmed, your house is live with a unique contract address.

---

## Step 3: Invite Your Members

After deployment, you'll land on your House page. Copy the **invite link** and share it with your group via WhatsApp, Telegram, or any messaging app.

When a member opens the invite link:

1. They see the house details (name, contribution amount, schedule)

2. They click **Join House**

3. If they have a wallet: connect and sign the enrollment transaction

4. If they use MOMO: they provide their phone number for payment notifications

Members appear in the Members section of your house page once enrolled.

---

## Step 4: Run Your First Round

Once all members are enrolled, you (the organizer) can open Round 1 by clicking **Start Round**. This sets the payout recipient (based on the order agreed at creation) and opens the contribution window.

**Members receive a notification**:

> "Round 1 is now open. Contribute 50 USDC (or 32,750 XAF via MTN MOMO) by April 15, 2026. On-time contributions earn 100 $NKAP."

Members pay via their chosen method. The progress bar on the house page updates in real time as contributions arrive.

When all members have paid, the contract automatically disburses the pool to the round recipient. No manual action required from the organizer.

---

## Step 5: Track Your Circle

The **Dashboard** at `/app/dashboard` shows:

- All your active houses

- Your NKAP balance and reward history

- Your contribution streak

- Your NFT badges

- Upcoming deadlines

---

## Tips for a Successful House

**Choose members you trust.** Smart contracts enforce payment logic, but your group's social cohesion matters. Start with people who have a track record of reliability.

**Agree on payout order before launching.** The order is written into the contract at creation. Discuss who goes first — often determined by who needs the money most urgently.

**Set a realistic contribution amount.** It should be enough to matter but not so much that it strains members. A common first house: 25–100 USDC per month.

**Enable notifications.** The platform sends WhatsApp/SMS reminders 7 days, 3 days, and 1 day before deadlines.

**Start small.** Run a 3- or 4-person circle for the first round. Once everyone is comfortable, expand.

---

*Ready? [Create your first house now →](/app/houses/create)*

---

### How We Earn Yield on Your Pool: A Technical Deep-Dive into Our Aave v3 Integration

URL: https://njangi.xyz/blog/defi-yield-aave

Author: Njangi House Engineering

Role: Protocol Team

Category: DeFi

Published: 2026-03-12T00:00:00Z

Updated: 2026-03-12T00:00:00Z

Read time: 7 min

Tags: DeFi, Aave, yield, Polygon, USDC, savings

Idle pool funds earn DeFi yield via Aave v3 on Polygon. Here's exactly how it works, the risks involved, and how yield is distributed.

## What is DeFi Yield?

In traditional banking, when you deposit money in a savings account, the bank lends that money to borrowers and pays you a small portion of the interest (typically 0.01–0.5% APY). The bank keeps the majority.

In DeFi (Decentralized Finance), lending and borrowing happens via smart contracts without the bank intermediary. Lenders deposit assets into a liquidity pool. Borrowers take loans from the pool and pay interest. The interest flows directly to the lenders.

**Aave v3** is the leading DeFi lending protocol, operating on Polygon, Ethereum, Arbitrum, and other chains. In March 2026, USDC deposits on Aave Polygon earn approximately **4.5–6% APY** — dramatically better than traditional bank rates.

Njangi House's optional yield feature deposits idle pool funds into Aave v3, earning this yield for the benefit of house members.

## The Mechanics: How Pool Funds Work

A standard Njangi House round works like this:

- **Round opens**: Members begin contributing USDC

- **Collection period**: 4 weeks (for monthly frequency)

- **Payout execution**: When all members have paid, the pool is disbursed to the round recipient

During the collection period, there's a window where funds are "idle" — held in the contract but not yet disbursed. For a house with 6 members contributing 100 USDC each, the pool accumulates from $0 to $600 over the collection period, then sits at $600 until payout is executed.

Aave integration means this idle capital is put to work.

## The Smart Contract Integration

The integration uses Aave's `IPool` interface with two key operations:

### Supply (Deposit)

```solidity

function _depositToAave(uint256 amount) internal {

usdc.forceApprove(aavePool, amount);

try IAavePool(aavePool).supply(

address(usdc),

amount,

address(this),

0 // referral code

) {

emit YieldDeposited(amount);

} catch {

// Silently continue if Aave unavailable

}

}

```

When a member contributes USDC (if yield is enabled), the contract immediately approves the Aave pool and calls `supply()`. The USDC leaves the house contract and enters the Aave liquidity pool. In return, the house contract receives **aUSDC** — Aave's interest-bearing token.

### aTokens: The Key Mechanism

aUSDC (Aave USDC) is a 1:1 rebasing token. When you hold aUSDC, your balance increases automatically every second as interest accrues. If you deposit 100 USDC and the APY is 5%, after one year your aUSDC balance will be 105.

This is elegant: the house contract doesn't need to actively claim yield. It simply holds aUSDC, and the balance grows continuously.

### Withdraw (Payout + Yield)

```solidity

function _withdrawFromAave(uint256 amount) internal returns (uint256) {

try IAavePool(aavePool).withdraw(

address(usdc),

amount,

address(this)

) returns (uint256 withdrawn) {

emit YieldWithdrawn(amount, withdrawn > amount ? withdrawn - amount : 0);

return withdrawn;

} catch {

return amount;

}

}

```

When payout is executed, the contract withdraws from Aave. The `withdraw()` function returns the full balance including accrued yield. If the house deposited 600 USDC and accrued 2 USDC in yield during the collection period, the house receives 602 USDC back.

The extra 2 USDC is added to the payout — so the round recipient receives their full share plus a pro-rated share of the yield earned.

## Yield Distribution Model

In the current implementation, all yield earned during a round is added to the payout for that round's recipient. This means:

- Early round recipients (Round 1, 2) receive less yield (shorter collection period)

- Later round recipients (Round 5, 6) receive more yield (full collection period)

A future governance proposal will introduce **yield pooling** — where yield from all rounds is accumulated and distributed equally to all members at the end of the full cycle. This creates a fairer distribution and slightly increases the incentive for members in later payout positions.

## Risk Analysis

No DeFi integration is risk-free. We're transparent about the risks:

**Protocol risk**: Aave v3 is a battle-tested protocol with billions in TVL, multiple audits, and years of mainnet operation. However, no smart contract is 100% risk-free. An exploit in Aave could, in theory, affect deposited funds.

**Our mitigation**: Yield integration is **opt-in**. It must be explicitly enabled when creating a house. The majority of houses should run without yield integration. For yield-enabled houses, we recommend smaller contribution amounts to limit exposure.

**Liquidity risk**: Aave withdrawals can theoretically fail if the pool's utilization rate is extremely high (all available USDC is borrowed out). In practice, USDC pools on Polygon maintain >20% liquidity reserve.

**Our mitigation**: The `try/catch` wrapper in our smart contract means that if an Aave withdrawal fails, the transaction does not revert — the contract falls back to paying the payout from its direct USDC balance. Yield is lost, but principal is protected.

**Oracle/rate risk**: The APY on Aave fluctuates based on market demand. During low-utilization periods, APY can drop to 1–2%.

**Our mitigation**: Yield is a bonus, not a core promise. House contribution amounts and payout expectations are set without reference to yield. Any yield earned is additional.

## Real Numbers: What to Expect

At **5% APY** on Aave Polygon:

- Monthly collection period: 30 days

- Pool size: $600 USDC (6 members × $100)

- Average deployed duration: 15 days (accumulates from $0 to $600)

- Average deployed balance: $300

- Yield earned: $300 × 5% × (15/365) ≈ **$0.62**

At the scale of a typical house, yield contribution is small — a few cents to a few dollars per round. But across thousands of houses and larger contribution amounts, it adds up. And for members contributing hundreds of USDC monthly, the yield compounds meaningfully.

The bigger benefit is philosophical: by connecting African community savings to DeFi infrastructure, we're demonstrating that these communities have access to the same financial tools as anyone in the world.

## Enabling Yield for Your House

Yield integration is enabled at house creation and cannot be changed after deployment (to ensure all members know the rules when they join).

In the Create House wizard, Step 4 includes:

- Toggle: "Enable Aave yield on idle funds"

- Info tooltip explaining the mechanics and risks

- Warning: "Yield integration adds smart contract risk. Only enable if your members understand and accept this risk."

We recommend yield integration for experienced groups who are comfortable with DeFi. For first-time users, we recommend starting without yield and enabling it in a future house once comfortable with the platform.

---

*Learn more about our [security practices](/blog/smart-contract-audit) or [create a yield-enabled house](/app/houses/create).*

---

### Your Savings History as an NFT: How Njangi House Builds On-Chain Credit

URL: https://njangi.xyz/blog/nft-badge-system

Author: Njangi House Engineering

Role: Protocol Team

Category: NFTs

Published: 2026-03-10T00:00:00Z

Updated: 2026-03-10T00:00:00Z

Read time: 6 min

Tags: NFT, credit, badges, on-chain, reputation, Polygon

Every on-time contribution mints a dynamic NFT badge. Streaks unlock tiers from Bronze to Diamond — and your record follows you everywhere on-chain.

## The Problem with Financial Reputation

In traditional finance, creditworthiness is a number. A FICO score. A bank rating. A credit bureau report. These systems work reasonably well in countries with stable institutions and long financial histories — but they systematically exclude the billions of people who are "credit invisible."

Someone who has faithfully contributed to a savings circle for five years, never missing a payment, has demonstrated exactly the discipline a credit system is supposed to measure. But that history exists nowhere a bank can see it. It lives in WhatsApp group chats, in the memory of the circle organizer, in handwritten notebooks.

Njangi House changes that. Every contribution you make on our platform creates a permanent, verifiable, on-chain record. And that record is represented as a dynamic NFT.

## How the NFT Badge System Works

Our `NjangiNFT` contract is an ERC-721 (non-fungible token) that mints a unique badge for every significant on-chain action:

### Contribution Badges (`TYPE_CONTRIBUTION`)

Every time you make an on-time contribution to any Njangi House, a contribution badge is minted to your wallet. These badges are dynamic — their appearance and metadata evolve as your streak grows.

**Streak Tiers:**

| Streak | Tier | Badge Appearance |

|--------|------|-----------------|

| 1–2 contributions | Bronze | Warm bronze ring, simple design |

| 3–5 contributions | Silver | Silver ring with geometric pattern |

| 6–11 contributions | Gold | Gold ring with intricate filigree, glow effect |

| 12+ contributions | Diamond | Diamond ring with animated shimmer, full color |

The badge's SVG is generated entirely on-chain. There is no off-chain image hosting. The badge is fully self-contained — the metadata URI returns a Base64-encoded JSON that includes the SVG directly.

### Payout Badges (`TYPE_PAYOUT`)

When you "chop" — receive the pool — a special payout badge is minted. This badge records:

- The house name

- The round number

- The payout amount in USDC

- The date of the payout

Payout badges are proof that you participated in a complete circle and were a recipient.

## On-Chain SVG: Why It Matters

Most NFTs store their images on IPFS or a centralized server. When the server goes down or the IPFS pin expires, the image is gone — a phenomenon called "link rot" that has already affected thousands of NFT collections.

Njangi House NFTs store everything on-chain. The SVG artwork is generated by the smart contract in pure Solidity:

```solidity

function _generateSVG(

uint8 tier,

string memory streakStr,

string memory typeLabel

) internal pure returns (string memory) {

string memory tierColor = tier == 3

? '#b9f2ff' // Diamond

: tier == 2

? '#fbbf24' // Gold

: tier == 1

? '#94a3b8' // Silver

: '#cd9a5c'; // Bronze

return string(abi.encodePacked(

''

));

}

```

This SVG is then Base64-encoded and embedded directly in the token URI. Your badge will look the same in 10 years, 50 years, or 100 years — as long as the blockchain exists.

## The Metadata Structure

Each badge's metadata follows the ERC-721 metadata standard:

```json

{

"name": "Njangi Contribution Badge #247",

"description": "Gold tier — 8 consecutive on-time contributions to Njangi House circles",

"image": "data:image/svg+xml;base64,PHN2ZyB4bWxucz...",

"attributes": [

{ "trait_type": "Type", "value": "Contribution" },

{ "trait_type": "Tier", "value": "Gold" },

{ "trait_type": "Streak", "value": 8 },

{ "trait_type": "House", "value": "Famille Biya Savings" },

{ "trait_type": "Round", "value": 3 }

]

}

```

This metadata is also fully on-chain, generated by the contract's `tokenURI()` function.

## Building a Credit History

Here's where the vision extends beyond a pretty badge. Every badge in your wallet is a timestamped, verifiable, tamper-proof record of your financial behavior.

**What lenders can see:**

- How many contribution badges you hold (total activity)

- Your highest tier (Diamond = 12+ consecutive on-time payments)

- Payout badges (you completed full circles, received payouts)

- Timeline (how long you've been participating)

This is a credit profile that:

- Cannot be forged (blockchain immutability)

- Cannot be selectively hidden (public ledger)

- Is portable across platforms (ERC-721 standard)

- Works across borders (no country-specific institution needed)

We're in conversations with DeFi lending protocols about using Njangi NFT tier status as a collateral factor — allowing Diamond-tier holders to borrow at better rates based on their on-chain savings history.

## Transferability and Soulbound Design

Currently, Njangi contribution badges are **transferable** ERC-721 tokens. They can be held in any wallet and viewed on any NFT marketplace.

We are evaluating a **Soulbound** model for future versions — where contribution badges are permanently bound to the wallet that earned them and cannot be transferred. This would make them even more credible as a financial identity primitive, since they couldn't be purchased or transferred to create a misleading track record.

The decision will be made through $NKAP governance, giving the community a voice in how their credit history is designed.

## Viewing Your Badges

Your badges are visible:

- On your **Dashboard** at `/app/dashboard`

- On any NFT marketplace that supports Polygon (OpenSea, Rarible, etc.)

- By checking your wallet address directly on Polygon Amoy explorer

If you hold a Gold or Diamond badge, you'll see a special visual indicator on your House member profile — other members can see at a glance that you're a reliable contributor.

## The Bigger Picture

The njangi system has always been built on demonstrated trustworthiness. In its traditional form, that trust is held in human memory and social relationships. In Njangi House, it's held in cryptographic certainty on a public blockchain.

Your Diamond badge is your reputation. Your streak is your credit score. And unlike a FICO number controlled by a private company, it belongs to you — held in your wallet, visible to anyone, forever.

---

*Start building your on-chain savings history. [Create or join a house today →](/app/houses/create)*

---

### MTN Mobile Money Integration Arrives Q3 2026: No Crypto Wallet Required

URL: https://njangi.xyz/blog/momo-integration-q3-2026

Author: Njangi House Engineering

Role: Core Team

Category: MOMO

Published: 2026-03-08T00:00:00Z

Updated: 2026-03-08T00:00:00Z

Read time: 7 min

Tags: MOMO, MTN, Orange Money, oracle, XAF, USDC, bridge

Our oracle bridge lets anyone pay contributions via MTN MOMO or Orange Money — XAF automatically converted to USDC on-chain.

## The Biggest Barrier in African Web3

Ask anyone building fintech for Africa about their biggest challenge, and you'll hear the same answer: the last mile.

Getting money in and out of crypto in Africa requires a smartphone, a wallet app, an exchange account, sometimes KYC documentation, and a reliable internet connection. For the 400 million Africans who use mobile money as their primary financial tool, the path to Web3 participation is long and filled with friction.

At Njangi House, we believe that if your grandmother can dial *126# to pay for groceries, she should be able to participate in a Web3 savings circle just as easily. Our MOMO integration, launching Q3 2026, makes that possible.

## What is Mobile Money?

Mobile money (MOMO) allows users to store, send, and receive money via a SIM card-registered account — without a bank account. In Cameroon, **MTN Mobile Money** and **Orange Money** are the two dominant operators, with a combined user base of over 12 million active users as of 2025.

The system works through a USSD menu (those *126# codes) or dedicated apps, and allows transactions including:

- Person-to-person transfers

- Bill payments and airtime

- Merchant payments

- Bank-to-wallet and wallet-to-bank transfers

Mobile money is deeply embedded in daily African economic life. In Cameroon alone, over 10 million MOMO transactions occur daily.

## Our Oracle Architecture

Bridging mobile money to the blockchain requires a trusted intermediary — what we call an **oracle**. The Njangi oracle service runs on Google Cloud Run and acts as a verifiable relay between the mobile money network and our smart contracts.

Here's how it works technically:

### Step 1: Payment Detection

When a member sends MOMO to the designated Njangi House number, the Mobile Money operator sends a webhook to our oracle service. This webhook contains the transaction details: sender phone, amount, reference number, and timestamp.

### Step 2: Signature and Registration

The oracle verifies the webhook signature (using HMAC-SHA256 with the operator's shared secret). If valid, it calls `registerPayment()` on our `MomoOracle` smart contract, logging the payment on-chain before any USDC moves.

### Step 3: Exchange Rate Conversion

The oracle fetches the current XAF/USDC rate from the Yellow Card API. This rate is locked for 30 minutes to protect both the member and the house from price volatility during processing. The conversion uses the formula:

```

USDC amount = XAF amount × 10^6 / (XAF per USDC × 10^6)

```

The rate is also stored on-chain in the `MomoOracle` contract with a staleness threshold of 4 hours — if the rate hasn't been updated, the oracle rejects the transaction to prevent processing at stale prices.

### Step 4: USDC Relay

The oracle then calls `relayPayment()` on the `MomoOracle` contract, which transfers the equivalent USDC from the oracle's liquidity pool to the target `NjangiHouse` contract. The relay also verifies an ECDSA signature from the oracle's signing key, ensuring that only authorized relays are processed.

### Step 5: Anti-Replay Protection

Each MOMO transaction reference (e.g., `CM-MTN-2026-03-01-ABC123`) is stored on-chain in a mapping. If the same reference appears twice, the contract rejects the second call. This prevents double-counting of payments.

## The ECDSA Security Model

A core concern with any oracle design is: what if the oracle is compromised? Our security model addresses this through layered protections:

**On-chain signature verification**: Every payment relay includes an ECDSA signature from the oracle's private key. The private key is stored in Google Cloud Secret Manager and never touches application memory directly. Even if an attacker gained access to the oracle server, they couldn't forge valid signatures without the private key.

**Staleness protection**: The exchange rate has a 4-hour validity window. An attacker cannot feed stale rates to extract value.

**Daily volume limits**: Each oracle relayer has a configurable daily USDC volume limit. Large payouts (>1,000 USDC) require multi-sig confirmation.

**Audit trail**: Every oracle action is logged to Firestore with full request/response details, enabling forensic analysis if anomalies are detected.

## The User Experience

For a member in Douala, the experience is familiar:

1. **Receive notification**: "Round 2 is open. Contribution: 25,000 XAF due by March 31."

2. **Open MTN MOMO app**: Tap "Send Money" or dial *126#

3. **Send to Njangi number**: Transfer 25,000 XAF to the designated house number

4. **Confirmation SMS**: Within 60 seconds, receive: "Njangi House: Payment received. 25,000 XAF = 38.17 USDC. Credited to Famille Biya Savings - Round 2. Ref: NJH-2026-03-XYZ"

5. **100 NKAP reward**: On-chain transaction mints NKAP to your wallet (if connected)

No app download required for paying via MOMO. No crypto wallet. No KYC beyond what MTN/Orange already have.

## Supported Operators and Regions at Launch

**Q3 2026 Launch:**

- MTN Mobile Money (Cameroon, Nigeria, Ghana, Rwanda, Uganda)

- Orange Money (Cameroon, Côte d'Ivoire, Senegal, Mali, Burkina Faso)

**Q4 2026 Expansion:**

- Airtel Money (Kenya, Tanzania, Zambia)

- M-Pesa (Kenya, Tanzania) via Daraja API

- Wave (Senegal, Côte d'Ivoire)

**Currency Support (via Yellow Card):**

- XAF (CFA Franc BEAC) → USDC

- GHS (Ghanaian Cedi) → USDC

- NGN (Nigerian Naira) → USDC

- KES (Kenyan Shilling) → USDC

- UGX (Ugandan Shilling) → USDC

## What This Means for Adoption

The MOMO integration removes the single biggest barrier to participation for the core demographic Njangi House serves. Consider the numbers:

- **400M+** mobile money users in sub-Saharan Africa

- **12M+** MTN MOMO users in Cameroon alone

- **60%** of Cameroonians use MOMO for regular payments